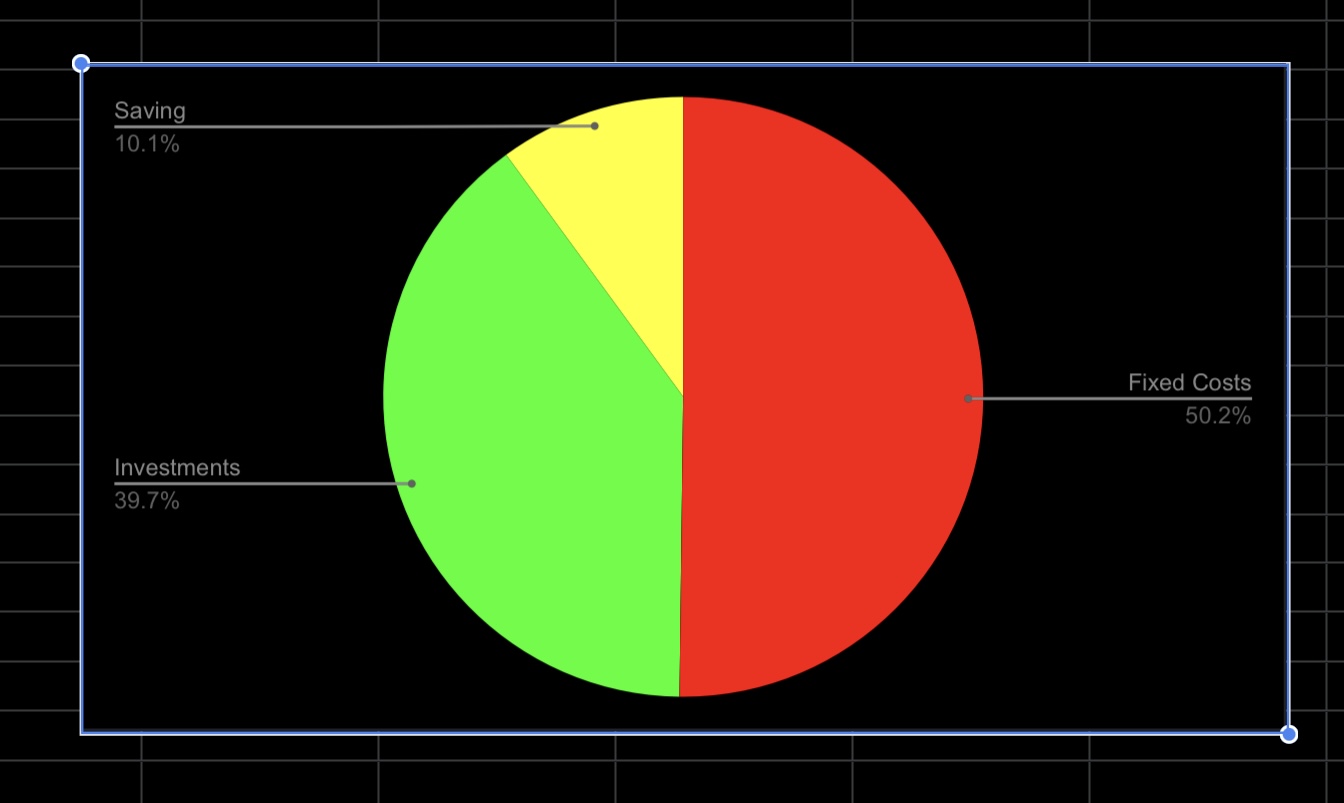

The 50/30/20 rule is a straightforward budgeting framework designed to help you manage your after-tax income by dividing it into three simple categories: Needs, Wants, and Savings/Debt Repayment. Here’s a detailed breakdown:

1. 50%: Needs (Essentials)

- What it covers: Expenses critical for survival and basic functioning.

- Examples:

- Rent/Mortgage payments

- Utilities (electricity, water, gas)

- Groceries (basic food, not dining out)

- Healthcare (insurance, essential medications)

- Minimum debt payments (e.g., car loan, student loan)

- Basic transportation (e.g., fuel, public transit)

- Key Rule: If missing this expense would severely disrupt your life, it’s a “Need.”

2. 30%: Wants (Lifestyle Choices)

- What it covers: Non-essential expenses that enhance your lifestyle.

- Examples:

- Dining out, takeout coffee

- Streaming services (Netflix, Spotify)

- Travel, hobbies, entertainment

- Luxury items (designer clothes, gadgets)

- Upgrades (e.g., a pricier apartment or car)

- Key Rule: If you can live without it, it’s a “Want.”

3. 20%: Savings & Debt Repayment

- What it covers: Building financial security and paying down debt.

- Examples:

- Emergency fund contributions

- Retirement savings (401(k), IRA)

- Investments (stocks, mutual funds)

- Extra debt payments (beyond minimums)

- Future goals (down payment, education fund)

Example Calculation

If your monthly take-home pay is $4,000:

- Needs (50%): $2,000

- Wants (30%): $1,200

- Savings/Debt (20%): $800

Pros & Cons

| Pros | Cons |

|---|---|

| but Simple to start | Rigid (may not fit high-cost areas) |

| Flexible for “Wants” | Oversimplifies “Needs” (e.g., groceries vs. dining) |

| Prioritaze savings | Doesn’t address high debt/income ratios |

Tips for Success

- Track expenses for 1–2 months to categorize realistically.

- Adjust ratios if needed (e.g., 60/20/20 in high-cost cities).

- Automate savings—direct-deposit 20% into a separate account.

- Review quarterly—life changes require budget tweaks!

Remember: The 50/30/20 rule is a guideline, not a law. Tailor it to your goals (e.g., aggressive debt payoff might mean 50/20/30 temporarily).

Alternatives to Explore

- 70/20/10: For those focusing on debt.

- Zero-Based Budgeting: Every dollar has a job.

- Envelope System: Cash-based spending control.

Start by analyzing your last 3 months of spending—does your current split align with 50/30/20? If not, identify leaks (often in “Wants”) and redirect funds to savings!